Despite high wealth in region, Massachusetts seniors face economic challenges in retirement

Wealth Gaps in the Golden Years report notes wide wealth disparities, highlights importance of Social Security and other programs among seniors

May 1, 2025

Boston—A new report from Boston Indicators, in collaboration with the Center for Retirement Research at Boston College, finds that despite our region’s higher levels of wealth, a large share of Greater Boston seniors struggle to cover their basic needs around and in retirement. The report, entitled Wealth Gaps in the Golden Years: Economic Insecurity for Older Adults in a High-Cost State, finds the issue is especially fraught for low-wealth households in Massachusetts, 80 percent of whom have less than what they need to age in place.

The report, released today with an online event hosted by the Boston Foundation, used both quantitative and qualitative research to showcase the data and give a broader sense of what lower-income and lower-wealth seniors are doing to manage their finances in their later years.

“The reward of a comfortable, secure retirement is one of the unwritten expectations of the American worker – but for too many Massachusetts seniors, the combination of Social Security, retirement savings and other programs doesn’t quite cover what is needed,” said Luc Schuster, Executive Director of Boston Indicators, the research center at the Boston Foundation. “As a result, the low-income seniors we interviewed are forced to use an array of strategies to make ends meet.”

Laura D. Quinby from the Center for Retirement Research analyzed income and wealth data and found that, while senior households in Massachusetts have more resources than the rest of the U.S., on average, these resources are not evenly distributed. While senior households in the top third of the distribution in Massachusetts had an average of nearly $3.6 million in wealth, those in the bottom third had an average of just over $55,000. The gap was narrower in income, but still large, with the top third having incomes nearly five times that of the lowest third ($169,003 to $34,340).

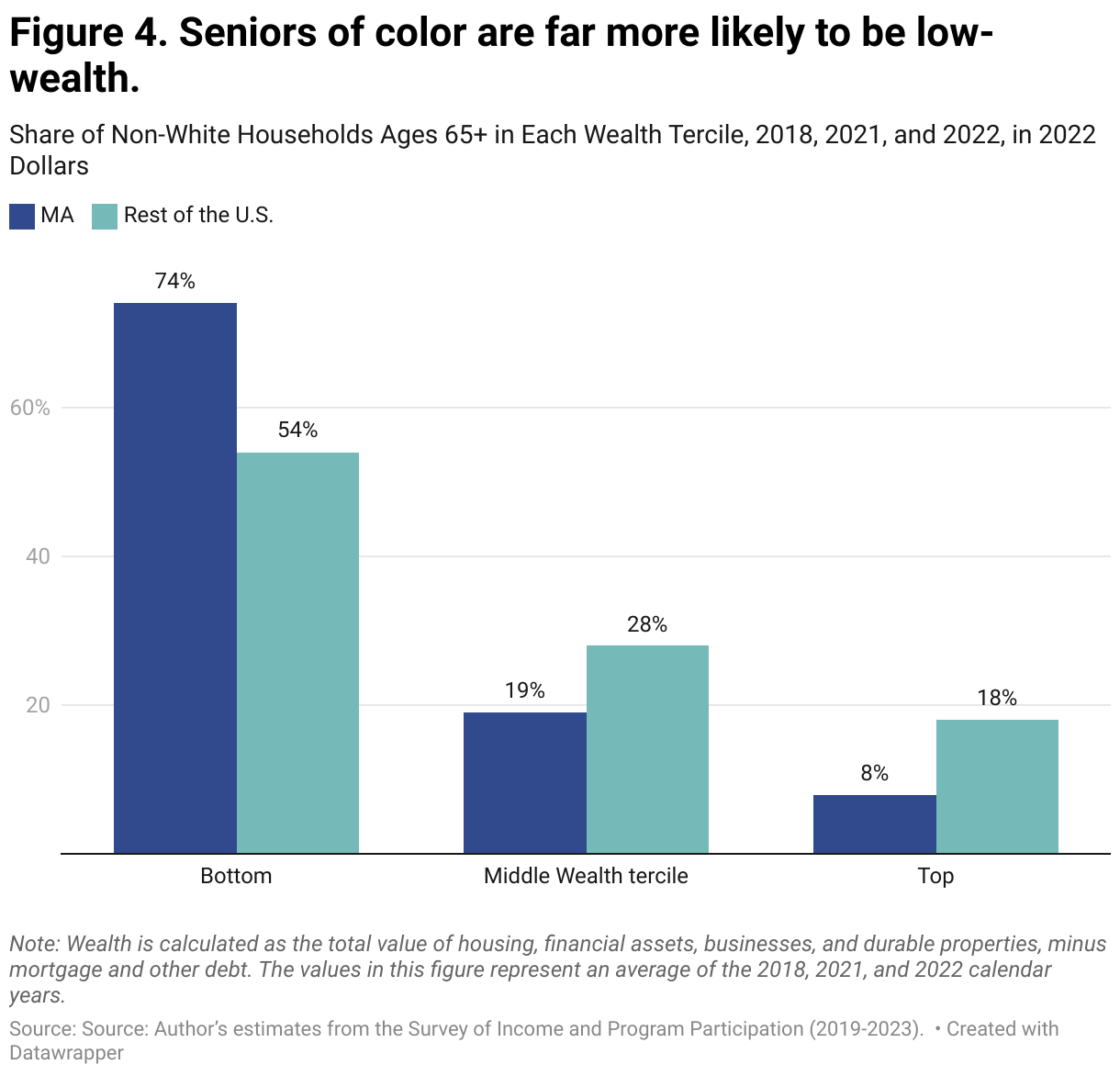

Quinby then compared older households’ financial resources with the local cost of living, using a sufficiency budget from the Elder Index, which is produced by the Gerontology Institute at the University of Massachusetts Boston. The analysis found that about 80% of seniors with lower levels of wealth in Massachusetts had insufficient income to meet their basic needs, significantly worse than the national share of 63%. The burden posed by Massachusetts’ high cost of living hits older households of color particularly hard, with 74 percent of non-White older households in Massachusetts falling into the bottom third of the Commonwealth’s senior wealth distribution, compared to only 54 percent in other states. And 76 percent of non-White senior households have income below the self-sufficiency budget, versus 52% nationally.

“Although Massachusetts is relatively wealthy, its high cost of living creates challenges for many older households,” said Quinby. “In particular, older households of color often have insufficient incomes to meet their basic needs and age in place without assistance.”

How lower-income seniors manage their resources was a core focus of the interviews conducted with 29 Greater Boston seniors. The interviews found that without savings and other earnings to fall back on, lower-income seniors relied heavily on Social Security for their income. Even so, they were forced to reduce their standard of living from their working years and counted on benefits like subsidized housing and other public benefits as lifelines to make ends meet.

They noted that accessing those benefits could often be challenging, especially for non-English speakers and those without support networks to help them find and access resources.

The report closed by highlighting opportunities to strengthen older adults’ financial stability, focusing on two areas that repeatedly came up in the interviews.

First, because many homeowners cited property taxes as a significant pain point in affordability, the report recommends expanding access to deferred property tax payment programs for seniors, simplifying their enrollment, and shifting the financial burden of those programs from individual municipalities to the Commonwealth.

Second, the report suggests that expanding access to programs that facilitate retirement savings could have a significant impact. One example: the Secure Choice Savings Program—an automatic IRA program for employees without access to employer-sponsored retirement savings. Studies from the Center for Retirement Research find that a Massachusetts Secure Choice program could significantly reduce the number of workers approaching retirement with little to no savings and would not pose a long-run burden to the Commonwealth’s budget.

The full report is available now for download at bostonindicators.org.